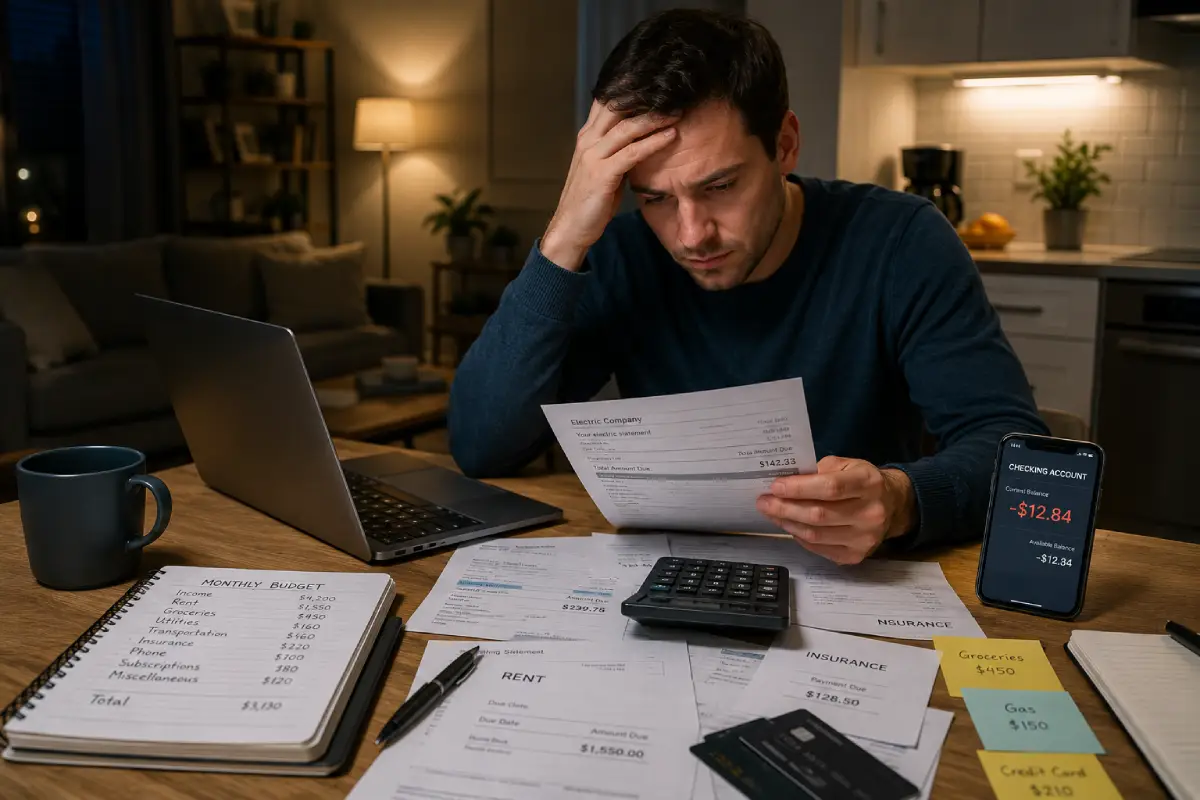

For millions of Americans, payday brings a brief sense of relief.

Bills get paid, the checking account finally looks healthy again, and for a few days it feels like everything is under control. But as the month moves on, that balance slowly disappears. Rent, groceries, insurance, transportation, subscriptions, and everyday purchases quietly consume the paycheck until there’s little—or nothing—left before the next one arrives.

Eventually, the cycle repeats.

Living paycheck to paycheck isn’t always a sign of poor financial decisions. In many cases, it’s the result of rising housing costs, inflation, healthcare expenses, student loans, or wages that haven’t kept pace with the cost of living. People across every income level experience it, including professionals with six-figure salaries.

The problem isn’t necessarily how much money you earn. Often, it’s how little room exists between your income and your monthly obligations.

What does living paycheck to paycheck really mean?

The phrase is frequently misunderstood.

It doesn’t simply mean having a low income. It means depending on your next paycheck to meet your current financial commitments.

If missing one paycheck would immediately make it difficult to pay rent, cover groceries, or keep up with monthly bills, you’re likely living paycheck to paycheck regardless of your salary.

Some households earn $45,000 a year and struggle.

Others earn more than $150,000 and experience exactly the same financial pressure because their expenses have grown alongside their income.

The common factor isn’t income—it’s the absence of financial breathing room.

Why higher income doesn’t always solve the problem

Many people believe a raise will automatically eliminate financial stress.

Sometimes it does.

But many households experience something known as lifestyle inflation. As income grows, spending grows with it. A larger apartment, newer car, more vacations, premium subscriptions, and frequent dining out gradually become part of everyday life.

Before long, the higher paycheck feels just as tight as the previous one.

Without intentional financial planning, increased income often creates a more expensive lifestyle rather than greater financial security.

The hidden cost of constant financial pressure

Living paycheck to paycheck affects far more than your bank account.

It influences daily decisions, career choices, relationships, and even physical health.

Unexpected expenses become emergencies.

Necessary repairs get postponed.

Retirement savings are delayed.

Credit cards become a temporary solution that often develops into long-term debt.

Over time, financial stress can create a cycle that’s difficult to escape because every setback reduces the ability to prepare for the next one.

Small changes can create breathing room

Escaping the paycheck-to-paycheck cycle rarely happens overnight.

For most people, it’s the result of gradually creating more space between income and expenses.

That may involve reducing recurring monthly costs, negotiating insurance premiums, refinancing expensive debt, increasing income through career development or freelance work, or simply becoming more intentional about discretionary spending.

Building even a modest emergency fund can change the entire equation.

Instead of relying on credit cards when something unexpected happens, savings provide time to respond without immediately creating new debt.

Progress usually begins with small improvements rather than dramatic transformations.

Focus on building margin, not perfection

Many budgeting articles encourage people to cut every non-essential expense.

While reducing unnecessary spending can certainly help, sustainable financial progress comes from creating margin—not eliminating everything enjoyable.

A realistic budget should include room for entertainment, hobbies, and occasional treats.

Financial plans fail when they become impossible to live with.

The objective isn’t to build the cheapest possible lifestyle.

It’s to build one that’s financially sustainable.

Financial freedom starts with one extra dollar

One extra dollar left at the end of the month may not seem significant.

But it represents something much more important.

It means your money is beginning to work for you instead of disappearing as quickly as it arrives.

That extra dollar eventually becomes twenty.

Twenty becomes two hundred.

Two hundred becomes the beginning of an emergency fund.

Every financially stable household started somewhere.

Breaking the paycheck-to-paycheck cycle isn’t about becoming rich overnight.

It’s about slowly creating choices where previously there were none.

Financial freedom isn’t built in a single paycheck.

It’s built through hundreds of intentional decisions that gradually give you more control over your future.